An Illustrated Guide to Auction House Terminology

What is “chandelier bidding?” How do third-party guarantees work? And what are the “three D’s?”

Over the course of a single week in November 2014, over $1 billion was spent on contemporary art at the three largest auction houses — Christie’s, Sotheby’s, and Phillips. Despite endless articles on the state of the art market, the actual mechanics of the auction world are largely opaque. What is “chandelier bidding?” How exactly do third-party guarantees work? And what are the “three D’s?” Learn the basics with our terminology guide.

Consignor

An individual who entrusts the sale of their property to an auction house. The consignor retains ownership of their property until after it is sold.

Appraisal

An appraisal is the auction house’s evaluation of a work’s market or insurance value.

Lot

A lot is an object or group of objects for sale. An auction is comprised of multiple lots, each the subject of their own round of bidding.

Estimates

Low and high estimates are educated guesses by an auction house about how much a work is likely to sell for.

They should not be taken as an indication of a work’s value. Estimates are finely calibrated to encourage bidding. They also serve a useful PR purpose. High estimates can cement the belief that an artist’s work commands high prices. Lots can also be purposely underestimated. If such a lot then sells for a higher price, the auction house can boast a bullish interest in a particular artist and/or record prices.

Increment

The minimum incremental amount required of an under bidder in order to top the previous bid. Increments are standardized ahead of a sale, though in some cases the auctioneer has the discretion to modify or accept alternative increments.

Bidder Number

(aka: Paddle Number)

A number issued to each bidder. Attendees must register for a number ahead of an auction.

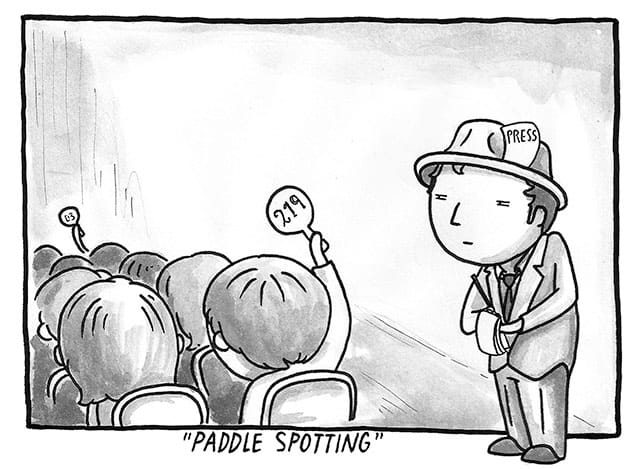

Paddle Spotting

The act of observing paddle numbers in order to identify who is bidding.

Absentee Bid

(aka: Written bid. Order bid. Commission bid)

A fixed bid submitted in advance of the auction.

Proxy Bid

A bid made on behalf of another individual. Requires advance registration.

Hammer Price

The price at which the auctioneer’s hammer falls (i.e. the winning bid).

The Hammer price does not include other fees such as the buyer’s premium, resale royalty, or additional taxes.

Resale Royalty

(aka: Artist Resale Right. Droit de Suite)

An artist resale royalty (ARR) is a percentage of the hammer price that must be paid to the artist who created the artwork on sale, or to their estate.

Although ARR’S are standardized in the European Union and legislated for in numerous countries around the globe, the US still has no such law in place, largely thanks to the lobbying efforts of the major auction houses. The American Royalties Too Act (ART) was recently reintroduced to Congress for consideration. You can read Hyperallergic’s Illustrated Guide to Artist Resale Royalties here.

Seller’s Commission

(aka: Seller’s Fee)

A commission paid by the consignor to the auction house.

The fee is usually a percentage of the hammer price. In some cases, an auction house may offer to waive the seller’s commission in order to attain prominent and desirable works.

Buyer’s Premium

(aka: Buyer’s Fee)

This is an additional charge — usually a percentage of the hammer price — that must be paid by the winning bidder to the auction house.

The buyer’s premium can range from anywhere between 12–25%. The percentage operates on a sliding scale depending on the price bracket of the object sold. Now commonplace, buyer’s premiums were widely criticized in the wake of their introduction by Sotheby’s (then Sotheby Parke Bernet) and Christie’s in 1975. The premium may be discounted for individuals whose consignments and/or purchases exceed a certain annual value, though the details of such deals are closely guarded.

Reserve Price

(aka: Upset price)

The reserve is the minimum, undisclosed price that a consignor is willing to accept for a work. If bidding fails to reach the reserve amount, then the work is “bought-in.”

Bought-in

(aka: Withdrawn. Passed)

This is the term used for when a work goes unsold, usually because bidding failed to reach the reserve price.

The consignor can try their luck at a later auction or consign their work to an auction house’s private sales department. Interested parties will often enquire after bought-in works in the days following an auction. If a work goes unsold, the consignor may be charged various fees (storage, shipping, promotional costs). The potential to incur such costs incentivizes consignors to lower their desired reserve price.

Burned

A colloquial term used to describe a lot that fails to sell or is sold for a price far lower than expected, the implication being that the future value of the item might have been adversely effected.

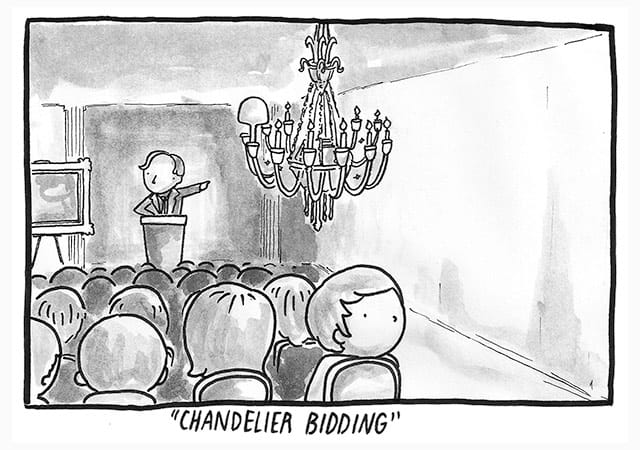

Chandelier Bidding

(aka: Rafter bidding. Off-the-wall bidding. Consecutive bidding. Vendor bid. Consignor Bid.)

A practice where the auctioneer pretends to take a bid from the room in order to encourage bidding, create the appearance of demand, or to push bidding closer to the reserve price.

Chandelier bidding is legal, as long as such bids stop short of the reserve. Auction houses prefer to describe the practice with the blander term “consecutive bidding.” The terms and conditions section of an auction catalogue will typically state that the house may place consecutive bids on behalf of a consignor. Auction houses claim that the practice promotes competitiveness and that if bidders knew the reserve price they would be less inclined to bid beyond it. Critics argue that chandelier bidding is deceptive and distorts the true level of interest for a particular lot.

Former democrat assemblyman Richard Brodsky spent 19 years attempting to ban chandelier bidding. After his ninth bill finally passed through the Assembly in 2007, it was subsequently quashed in the Senate. Republican State Senator John Flanagan also attempted to pass a companion bill in 2007.

Guarantee

(aka: Minimum price guarantee. Naked guarantee)

A guarantee is a specific amount that the auction house promises to pay the seller should their lot fail to sell or attain a particular price. The auction house can thus guarantee to the seller that their work will be sold.

Guarantees are a useful means of assuaging nervous consignors to commit prominent works to auction. They can however prove to be very costly. An auction house’s profits can be severely cut by having to pay out guarantees. On the other hand, the house may take a cut of a sale if it exceeds their minimum guarantee. In recent years, auction houses have increasingly turned to third parties guarantors in order to offset their own potential losses.

Third-party Guarantee

(aka: Risk sharing arrangements. Irrevocable bids)

Third-party guarantors are individuals or companies who promise to purchase a lot ahead of an auction for a specific, undisclosed amount.

If the work sells at auction for a price higher than the guarantee, the auction house may pay the guarantor a cut of the proceeds — typically described as a “financing fee” — by way of gratitude. The identities of third party guarantors are never disclosed. Lots that have third-party guarantors are usually marked by a symbol in the auction catalogue (Christie’s uses a diamond, Phillips uses a circle, and Sotheby’s uses two backward ‘C’s). Publicly identified third-party guarantors include Steve Cohen, Steve Wynn, and Peter Brant.

The three major auction houses have differing policies:

- Christie’s refers to third-party guarantees as “risk sharing arrangements.” Their terms and conditions state that third party guarantors will be paid a “risk fee” regardless of “whether or not the third party is the successful bidder.” The amount that Christie’s pays out in guarantees is the subject of intense speculation, since unlike Sotheby’s, Christie’s is a privately held company.

- Sotheby’s refers to third-party guarantees as “irrevocable bids.” Their terms and conditions state that irrevocable bidders are only compensated “in the event that he or she is not a successful bidder.”

- A spokesperson for Phillips told Hyperallergic that third-party guarantors are compensated when the sale of a work exceeds the amount guaranteed.

Third-party guarantees are the most controversial component of modern day auctions, primarily because guarantors are usually permitted to bid. Critics argue that this effectively allows for wealthy collectors to support the value of their collections, whilst potentially being paid for doing so. For this reason, many collectors maintain that it is unfair for the identities of third-party guarantors to be kept a secret.

If a third-party guarantor places a winning bid above the price of their guarantee at Christie’s or Phillips, they would effectively receive a discount on the lot via their cut of the sale’s proceeds. In these cases, the actual price realized for such works is obscured since the third party guarantor ends up paying less than the final publicly listed hammer price.

Third party arrangements are increasingly becoming more complex. The Art Newspaper’s Charlotte Burns recently reported on “third-party partners,” a new term devised by Christie’s to describe “individuals who take a stake in a Christie’s in-house guarantee.”

Collusion

Broadly defined as an illegal instance in which a number of bidders cooperate for their mutual benefit.

Bidders who share the same interests may form illegal “rings” whereby they bid against outsiders in an attempt to bring prices down. Buyers and sellers may also work together to boost the market value of particular artists, the worst case scenario being that one of them may achieve the wining bid and must pay for the lot, in which case, the value of other works by the same artist is perceived to have increased anyway. It is generally assumed that collectors regularly cooperate to boost prices, though it is difficult to definitively prove.

Shills

(aka: Potted Plants)

Individuals who drive prices up with phony bids (often referred to as “dummy” or “ghost” bids).

Bid Catcher

(aka: Bid Catcher. Bid Assistant. Bid Spotter, Ringman)

Bid Catchers are auction house employees who relay bids made on the auction house floor to the auctioneer.

New Money

An individual who enters late into bidding.

Fair Warning

A phrase used by the auctioneer to indicate that bidding is about to close.

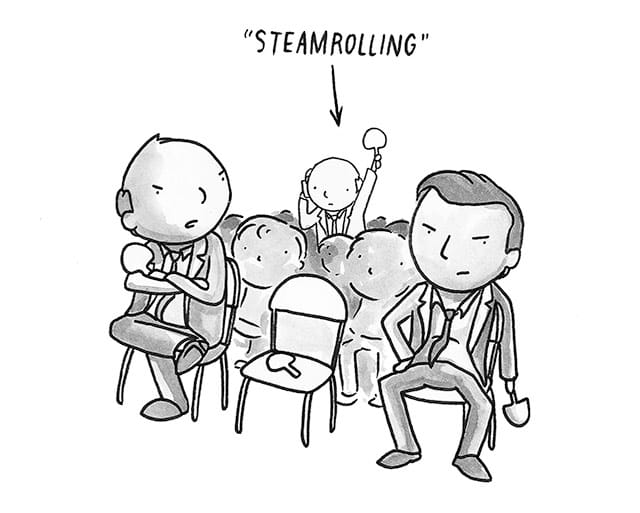

Steamrolling

When a bidder keeps their arm or paddle raised in order to make successive bids. An aggressive bidding tactic used to deter other prospective bidders.

Knocked Down

A phrase used by the auctioneer to indicate that a lot has sold. “Knock” refers to the auctioneer’s hammering of the gavel. I.e. “knocked down at $220,000.”

White Glove Sale

A term given to an auction in which every single lot was successfully sold — a rare occasion. The term possibly derives from the phrase “the white glove treatment” (i.e. special) whilst also referring to the gloves used to handle and exhibit work at the auction block.

Buy-In-Rate

The percentage of lots that failed to sell in a given auction.

Sell-Through Rate

(aka: Clearance Rate)

An assessment of an auction’s performance based on the percentage of lots sold.

Cover Lot

The work which appears on the front of the auction catalogue, typically touted as the most coveted or desirable lot. Auction houses will promise catalogue covers to the owners of sought-after works or to appease demanding sellers.

The Three D’s (Death, Divorce, and Debt)

Considered to be the three key circumstances from which collectors will consign works to auction.