Artists Are Not Kale: A Gallery Management Guide’s Many Failures

The it-book of summer, we were told, was Management of Art Galleries by the self-proclaimed “art market expert, serial entrepreneur, and bestselling author” Magnus Resch.

1. “This book is a lemon,” by Magdalena Sawon, Postmasters Gallery

“At its best, the art gallery is a creative enterprise that transcends business.”

“Art dealers who focus less on business and more on art are generally the dealers who become most successful and influential.”

—Jeffrey Deitch, from the introduction to Management of Art Galleries

When Jeffrey Deitch’s introduction to a book is the most intelligent, sensible, pro-art statement that runs 100% counter to the author’s vision, you know you’re in trouble.

The it-book of summer, we were told, was Management of Art Galleries by the self-proclaimed “art market expert, serial entrepreneur, and bestselling author” Magnus Resch. Not only does Resch’s heavily promoted book not contain any secrets about managing an art gallery, it’s not even a book. Magnus’s opus is rather a painfully padded pamphlet with fugue-like repeats of the same data and arguments. So it did not take long to read and annotate all 152 pages of Management of Art Galleries, which are set in large, generously spaced type for the visually impaired, and stuffed with endlessly described “diagrams” for the intellectually slow.

Resch has received great attention for his claim of developing “an economically sound and sustainable model for art galleries” based on 10 years of research. His top discovery is this: “One of the revelations from my survey was that galleries operating in the secondary market usually make higher profits.” Anyone with a passing knowledge of the art market already knew this. No, I do not have a PhD in economics. I have run a reasonably visible gallery for 30 years and I’m an art historian, the exact breed that Resch would like to see eliminated from the art galleries.

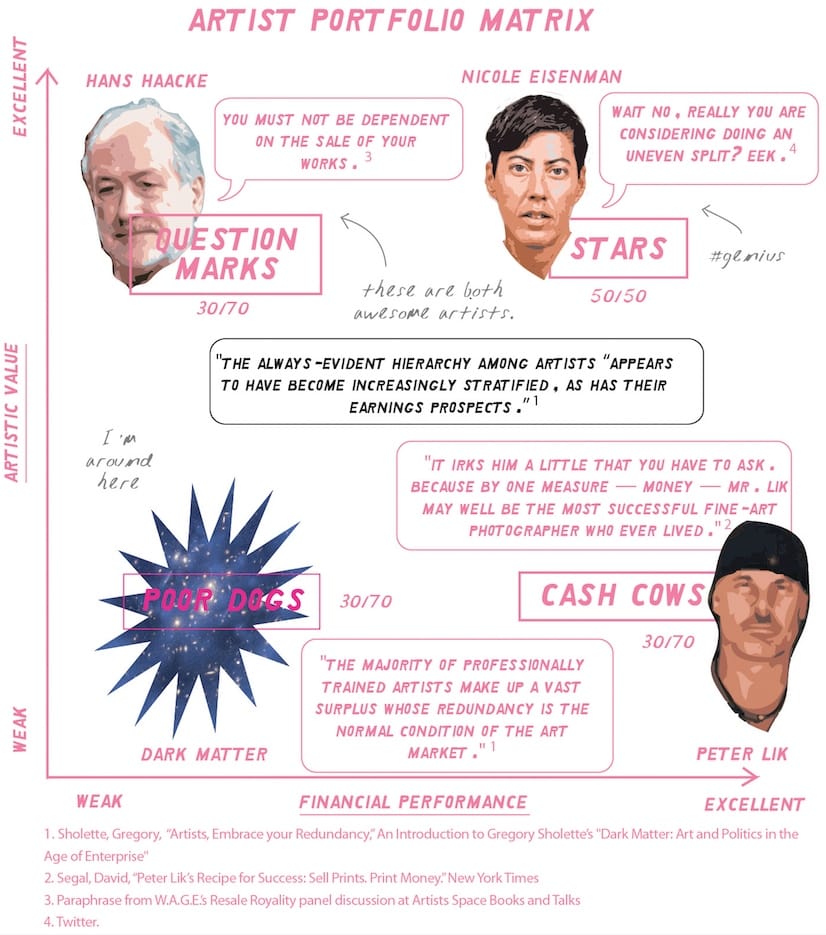

But it is the artists, the very foundation and the reason for art businesses to exist, who are the most shortchanged in Management of Art Galleries. Artists, who participate only in the primary sales segment of the market, are smugly sorted into four groups as — get this — poor dogs, question marks, stars, and cash cows. Resch did not even invent these groupings, they are ripped off from the “growth share matrix” (aka the Boston matrix) for identifying corporate profit categories. The result is a crude, pedestrian application of this business model onto a very slippery entity — artists. Resch’s proposals call for putting all risk — a legitimate component of any business endeavor — squarely on their shoulders: artists should get lower commissions, not be informed who the buyer is, and gift the dealer art in exchange for museum contacts. It’s toxic, exploitative, and embarrassing.

It is true that many galleries cling to a strained business model. However, most of Resch’s solutions are Business 101 — common sense and no-brainers — except when they’re spectacularly stupid (happy hour discount sales, sparklers, franchises, put an artist in a zoo — yes really). Not much is said about glaringly obvious areas of engagement for brick-and-mortar operations, such as art fairs, online business platforms, and social media or publicity outlets — elements that should dominate any analysis of how galleries should be responding to the current reality. Adaptability is a basic facet of intelligence and survival. Change is a given.

Dr. Resch, “the respected influencer in the art world, both as professor and entrepreneur,” offers the art world precious little beyond management efficiency, branding, and emphasizing art as product. Resch’s most elaborate conceit, a proposed three-tier gallery model, is largely unattainable.

Art is a moving target. Its cultural resonance and evaluation are never fully reflected in the facile metrics of the market. Galleries are a part of a larger social system. Words like community, audience, criticism, meaning, and culture are either distorted beyond recognition or entirely absent from Resch’s analysis. It’s a business-first headlong dive based on this premise: galleries should be taken away from people like me — fucking art historians — because art management grads are the future.

At the risk of being dismissed as naïve, I’ll repeat: it takes eyes, ears, brains, and passion — not an art market degree — to run a culturally meaningful gallery. The problem with the ever-growing barrage of marketing schemes lies in the sentence they all open with: “Art is like any other business.” It isn’t. No two artists require the same approach; I have as many hats as I have artists. If only I was in the business of selling hats.

As the mainstream media propagates breathless, uncritical market kibitzing, it may seem that at this moment the Pathology of Profit (capitalism at its most predatory) is an exclusive measure of success and value. Art is perceived as a commodity, a trophy, an asset class of bling. The proliferation of peripheral fields devised to skim money from the “art industrial complex” and its wealthiest habitués is as sure a sign of a bubble as the sixth Groupon clone. Everybody around art is an entrepreneur: we have concierge VIP services (Cultivist), mutual funds for art (Arthena), money loaning for art acquisitions (too many to list, starting with the auction houses themselves), and the holiest market grail, the algorithm (Artrank), to identify those foolproof profits.

To counter that, let me share a few of the guiding principles that are important at Postmasters:

- We want to afford ourselves the opportunity to show art that the market is not yet swallowing whole.

- We want to continue championing work with challenging but relevant content that may take time to be loved, appreciated, and acquired.

- We want to look for art by artists — old and young — that confounds us, that we don’t know or understand.

- We don’t want to anticipate the market and try to deliver on its demands. We want to challenge the market and perhaps teach it. We have, after all, sold some impossible things in the past.

- We want to search deep and wide for collectors who share this vision.

We are still here. Somebody gave the wrong guy a PhD.

2. “Management Be Afraid,” by William Powhida, Artist

“The best of these aspiring dealers intuitively understand that running a gallery is not just a business; it is a life.”

—Jeffrey Deitch, from the introduction to Management of Art Galleries

So, what is Resch’s plan for you, aspiring gallerist? Let’s imagine how Resch’s “threefold plan,” his tripod for vertical integration, might play out, since he does not include a timeline for his new model, which is based on a nine-point business plan borrowed from his PhD thesis advisor, Thomas Bieger. Apparently, it’s just supposed to happen all at once.

2.1 Fantasy Island: The Garage

The first thing you need to do on your way to becoming the next David Zwirner is to open a “Garage,” like Clearing’s industrial space in Bushwick that offers an authentic “truck repair experience” on the cheaper outskirts of a major city, but you shouldn’t expect to make any profit during this leg of your journey. In fact, your garage should be a nonprofit to start cultivating promising young artists, who you’re going to need later, but first you have to weed out the poor dogs from your question marks and stars. If you aren’t independently wealthy, you’ll have to find an investor during this phase of your vertical integration. My suggestion is that you frame your garage as an “art start-up” that will eventually yield an 18% profit margin like the most successful galleries in the world. Show your investors the graph on page 30 and ask them for three to five years of funding. It’s that easy.

2.2 Fantasy Island: The Gallery

After you’ve successfully created a vital, dynamic garage that has captured the imaginations of your art world visitors — which Resch breaks down into the opening crowd, art enthusiasts, collectors, walk-ins, and arts professionals — you’re going to move on to phase two of the plan, which is to open a “Gallery.” The gallery is where you are going to finally capitalize on the successful word-of-mouth reputation you have developed at your nonprofit garage by representing one to four of the artists you have carefully nurtured with your authentic “communication concept” for the non-buying, beer-swilling crowd of visitors like art critics. Personally, I suggest you invite people with popular Instragram accounts and give away free selfie sticks. People love selfies. Anyway, it is time to reap the rewards of the credibility you have have developed through dozens of exhibitions back at the garage.

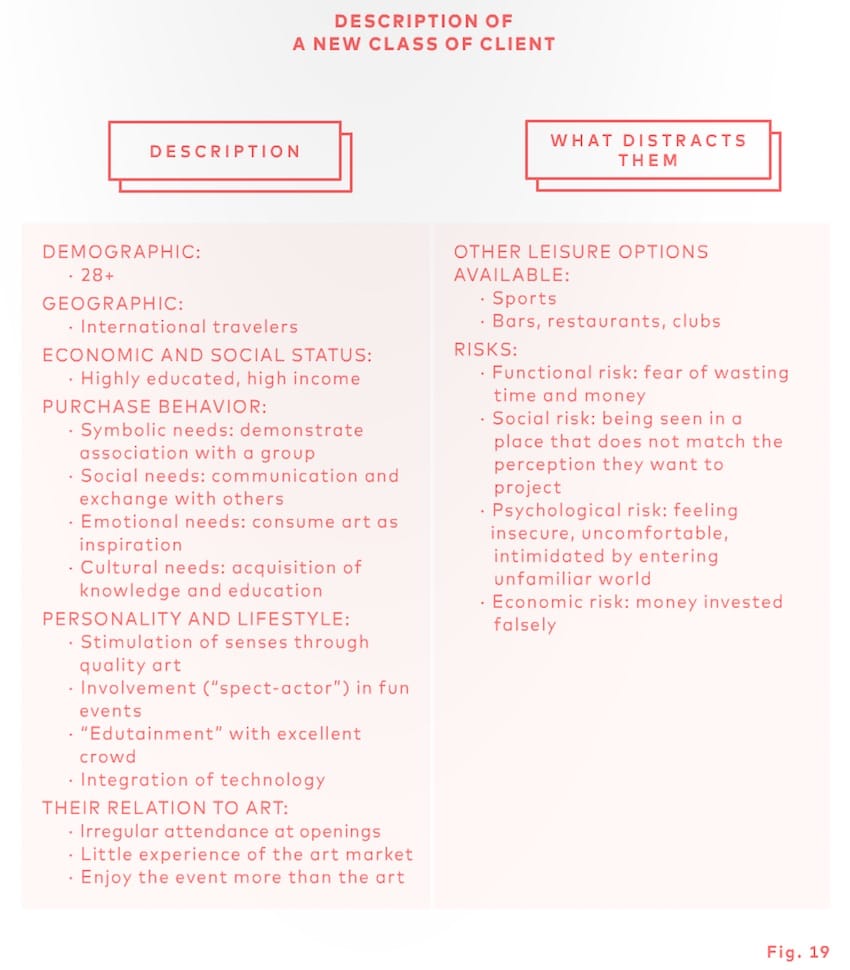

You should open your new carefully branded gallery, Artbox™, in a nicer space (keep expansion and parking in mind) in a trendy yet lower-rent area like the Lower East Side or the East End of London, where you are free to start selling art with your newly minted for-profit business. Resch doesn’t offer any specifics like forming an LLC, but that varies between the US, the UK, and Germany. (Germany has many publicly funded Kunsthalles, which Resch used as inspiration for his non-profit garage model.) Now it’s time to do business at ArtBox™ so you can earn some revenue to start paying off your investors and pay your full- and part-time staff. Your gallery’s brand should be instantly recognizable to both today’s aging male collectors (70% of them) and tomorrow’s promising customer concept — the youthful, 28-and-over internationally mobile millennials who have learned about your new gallery through positive feedback from their shabbier friends in the opening crowds. (Section 5.5 of Management of Art Galleries goes into some detail about Resch’s plan to capture the children of the aging collector base and their inherited wealth.)

At ArtBox™ you and your small staff of educated arts management graduates, like the ones Resch teaches at Leuphana University in Germany, should start doing brisk business with your one to four homegrown stars. (Resch’s “Competence Configuration” section, 5.9, explains why galleries should only hire arts management graduates and stop employing art history graduates who are apparently useless in his sad new world.) You should show a few of your unrepresented question marks from the garage to round out the rest of your exhibition calendar. You might even consider borrowing another star from ArtCube™, a competitor gallery in a different country, which might qualify as a cooperation concept as outlined in section 5.10. I’d also suggest you keep a couple more question marks hanging around to fill up all of the art fair booths that Resch recommends you pay out for, but you don’t have to represent them.

Now that ArtBox™ is up and running, you’re going to spend the next few years charming 28-and-over millennials and help them overcome their fears of embarrassment about buying work by providing edutainment (like those free selfie-sticks), while you manage the careers of your one to four stars. This will be easier if you’ve developed four Oscar Murillos™, whose prices have skyrocketed at auction since they debuted at the garage. But if any of your stars start lagging or showing signs of turning into poor dogs or question marks you should cut their commissions to 30% or dump them like Sadie Coles to keep your stable fresh, timely, and trouble-free. You can’t be bothered with dealing with difficult artists!

Meanwhile, you should remain wary of poachers at established Blue Chips and have your artists locked down with iron-clad contracts. You don’t want to lose your Murillo™ to David Zwirner like Carlos/Ishikawa. Maybe you should keep a few more question marks hanging around after all, just in case someone figures out how to get out of that contract.

2.3 Fantasy Island: Fine Art

It’s 2025, Donald Trump has just left office and Kanye is having a delightful first year as President of the United States. You’re finally ready to complete your vertical integration by moving, after nearly a decade of making less than 10% profit off your primary market sales, into Fine Art. Now that you’ve got a stable of one to four stars, a few question marks, and a cash cow (an artist who seemingly appears out of thin air, sells a lot, and is quietly ridiculed for producing the same stale work over and over), you can move into the secondary market by offering an array of services including buying back work before it heads to auction, brokering private sales of your stars’ works between collectors (this is great news, because you get a 10–20% commission and you don’t have to give a penny of it to those greedy artist pigs you’ve toiled for all these years), and providing art restoration services for those non-archival cardboard pieces by some question mark you showed a few years ago.

2.4 Fantasy Island: Inevitable Success

Life is great, you followed Resch’s business model to a tee. You organized panels co-sponsored by Hyperallergic™ with experts like William Powhida and Magdalena Sawon and ran happy hours with steep art discounts (per Resch’s section 5.7, “Revenue Concept”) sponsored by Heineken™. You took Jeanne Greenberg-Rohatyn’s advice and packaged your less finicky stars with Levi’s™ (individualized conformity), Mercedes-Benz™ (performance luxury), and UBS™ (discrete Swiss banking services) to create that dynamic cooperation model you read about in section 5.10. Now you travel the globe looking for new, young artists in Western Africa to debut at the garage, because your full-time staff of 30 art management grads run the daily operations of your mega-gallery. You are free to cultivate your extensive secondary market network of maturing 38-and-over millennials who have accumulated an even greater amount of global wealth and are looking to park more of their money in mobile art commodities, art mutual funds, and the array of art investment services that ArtBox™ has partnered with over the years.

When you think back to that first year and to the day you followed Resch’s advice and left the garage door open and two young artists dropped in to help you build walls for free and install your show, you are awash in gratitude for the non-buying visitors who helped fuel your empire of ArtBox™ galleries. In fact, you’ve just sold your first Artbox™ franchise to a young entrepreneur in Beijing for a substantial licensing fee. Who could have imagined that you would rise to such heights based on the recommendations of Magnus Resch, best-selling author, with little or no money and $50,000 of student debt from your master’s degree in the art market?

3. The Reality Concept

While my timeline is ludicrous, what’s even more remarkable about Resch’s book is that all three steps of his plan are supposed to happen at once, like unfolding a tripod to take a picture of the world. The mysteriously funded aspiring gallerist will open a Garage, a Gallery, and Fine Art services all at once to better insulate themselves from “troughs in any one market.” Let’s be clear, the garage is a nonprofit. There’s no revenue ever coming in from the garage so it’s always a trough. It should be self-evident that Resch’s plan is unattainable because galleries do not emerge into existence, fully-formed, with one to four stars in any credible manner without relying on the work of other gallerists or institutions that helped start an artist’s career.

Ghanaian artist Ibrahim Mahama’s rapid rise to star status reveals both the curatorial and institutional support required to build a career and the risks of focusing so heavily on an artist’s market value. Greg Allen has done a spectacular job of leveling ur-manager Stefan Simchowitz’s claim in his $4.5-million lawsuit that he and partner “Ellis King” were solely responsible for creating a market for Mahama, who is being sued for invalidating 297 works of art. While Mahama has quickly gained visibility, from a Gasworks residency in London in 2013 to the 2015 Venice Biennale, his “artistic value” — which makes up half of Resch’s abysmal “Artist Portfolio Matrix” — still required the attention and interest of curators and institutions, not just Simchowitz’s “Trust Me Special” sale of Mahama’s installation practice stretched out into 3 sizes of paintings for the discerning collector. I don’t know Mahama’s reasoning for invalidating the works, but I suspect that if he were looking at Resch’s matrix, Mahama might have concerns about his artistic value being overshadowed or destroyed by the “financial performance” of the paintings he produced for Simchowitz and King.

While Resch only makes a passing reference to Simchowitz as a notorious “art flipper,” they both share the rather unfortunate distinction of being thought of as “disruptors” looking to shake up traditional practices with “new” models, which are not very new at all and often justify the exploitative, neoliberal logic of extracting wealth from everything. Simchowitz and Resch both believe in contracts for artists, and the Mahama case should serve as a clear warning for younger artists, whom Resch defines as the ideal artist for the garage — “under thirty, have only marginal experience in the art market.” In many ways I think Simchowitz’s business, Simcor, is a very real application of some of Resch’s worst ideas and generally reveals his very corporate vision of the art world.

4. Corporate Vision

Melanie Gerlis of the Art Newspaper wrote that Resch’s book doesn’t promote a corporate vision of the art world. On the contrary, executing his “threefold plan” would require an enormous amount of capital to execute all at once. His key characteristics and descriptions of gallery employees sound very similar to the work a committed gallerist should be doing himself. According to his job descriptions in figure 22, the gallery director should be “solely responsible for artist selection/curating” and at the Fine Art level the managing director should be “completely and solely responsible for running the fine art trade and artist selection.” What, then, is the gallerist in Resch’s model? I’m not quite sure, but it looks like a position ideally suited for a CEO like Gary Friedman at Restoration Hardware, whose RH Contemporary gallery closed earlier this month so the brand can be folded into something called RH Modern. Christie’s auction house also tried vertical integration with their Haunch of Venison galleries in New York and London. Apparently these operations did not involve a traditional gallerist, but hired directors and managers who lacked the personality to cultivate a credible brand.

The engineering of Resch’s tripod is all very logical and makes a great deal of sense on paper if you live in the fantastic world of Horatio Alger and believe in the power of luck and pluck to become the next art world patriarch like David Zwirner or Larry Gagosian. Unfortunately, one cannot manage personality, capital, and operate a machine that stops time. Resch’s plan is so silly and unrealistic because he’s simply describing three different stages of a gallery’s life cycle and trying to hedge the risks of running a gallery by merging them all into one big, false story that dispenses with the decades of work required to build a brand or establish a vision.

5. Art as Business

In many ways, a gallery is a kind of cultural cooperative where the sales of a few artists keep the whole thing afloat during the cyclical trends of art world relevance — post-internet today, post-inventory tomorrow. They are also, in the words of David Zwirner, “the craziest freebie in the world.” Often, the sales of two or three stars subsidize an entire season of art exhibitions by those problematic poor dogs and experimental question marks. As Sara Greenberger Rafferty remarked sarcastically on her private Twitter account, some artists are just “#windowdressing #imheretomakeyoulookgood.” This points to the interdependence of artists within a gallery, where we are lucky if there are one to four stars and a cash cow helping to fund the whole business. In Resch’s business plan there is no room for representing “window dressing” that adds to a gallery’s “artistic value.” In Resch’s art world only those one to four stars deserve a 50/50 split and ongoing representation, while everyone else is left in precarious situations, doing shows as independent contractors on a 30% commission. He seems to lack the basic understanding that Zwirner had back in 2013 after Hurricane Sandy flooded many Chelsea galleries — that the gallery system is a “giant freebie” for the public that floats poor dogs, question marks, and even cash cows. If our society valued corporate culture less, we might consider providing subsidies for garages and galleries, instead of relying on a for-profit system where 30% of galleries lose money while providing all that free access to opening crowds who can’t afford art. Or perhaps galleries should start charging all those non-paying freeloaders looking for happy hours money at the door.

This leads back to the inevitable question: how can 30% of galleries operate at a loss and many more operate with very little profit? There are many reasons that are not entirely rational or fair, including non-payment and partial payment to artists, gallerists who privately fund the gallery for social and cultural status, gallerists who quietly hold full-time day jobs, and gallerists risking a long-term investment for that success Resch’s plan tries to neatly wrap up in an instantly unfoldable tripod of success.

The fact that so many galleries can operate while losing money makes me question Resch’s research, including his interviews with 51 experts and his eight case studies of successful galleries. I wonder who those experts were and why they are not revealed to let us evaluate the “status of their expertise” or experience in the art world, as Sarah Thornton let us do in Seven Days in the Art World. Without knowing who Resch spoke with, we are left with eight minimalist case studies that superficially illustrate successful galleries and reveal little about their success beyond generic pablum like “Be original, and stay true to your belief of what good art is. Don’t follow the crowd” or “Think out of the box. Break the Rules.” These are the kinds of statements you find on inspirational posters, not in a book claiming exhaustive research into best practices.

Case Study: Invisible-Exports

Risa Needleman and Benjamin Tischer, co-founders and co-directors of Invisible-Exports, worked for a gallery that focused too heavily on one to four stars, and they realized they had a different vision of what a gallery could be. They found a backer, which is more likely after you’ve worked in the gallery system for years rather than just starting out with no connections or network, and opened their small Lower East Side space with the funding to operate for two years without any sales. They did not need Resch’s book to understand that profit cannot be the first and last motivation for a gallery, and that credibility isn’t built on a formula. They opened the gallery to support the work of artists like Genesis P-Orridge who they felt were underrepresented and creating important, necessary work. These ideas are counter-intuitive for a profit-margin seeking manager like Resch, whose primary markers of success are profitability and how many employees you have. That culture must operate like a business, if only to survive in a society indifferent and even hostile to art that challenges social and cultural norms, eludes Resch’s understanding. I suppose he, like many economists, operates on the assumption that everyone involved in the unlikely business of art is a rational actor unmotivated by passion, delusion, dreams, or even hope.

6. Value Proposition

So much of Management of Art Galleries is ultimately this kind of generic advice that Magdalena’s annotated reading included a “huh” and “duh” list detailing both the inane — hand out sparklers at openings whenever a sale is conducted, ask people to help install your shows for free, take more money from artists — and the ordinary — build your network, keep overhead low, take care of your artists (see the contradiction there?). Serial disruptor Kenny Schacter may be right in advising readers to take the book “with humor and 100 grains of salt,” but I worry that his pat dismissal elides Resch’s ugly implicit message, which is that artists are simply human capital to be raised, grown, and tended to in order to feed an industry. Artists are not kale. We are neither product, commodity, nor human capital, but complicated people who provide the foundation for the entire $61-billion art-industrial complex. The possibility of profits extracted by ancillary, service-oriented byproducts simply cannot coexist with the strange, traditional, experimental, crazy, rigorous, beautiful, meaningful, shallow, decorative objects, gestures, and performances that artists make.

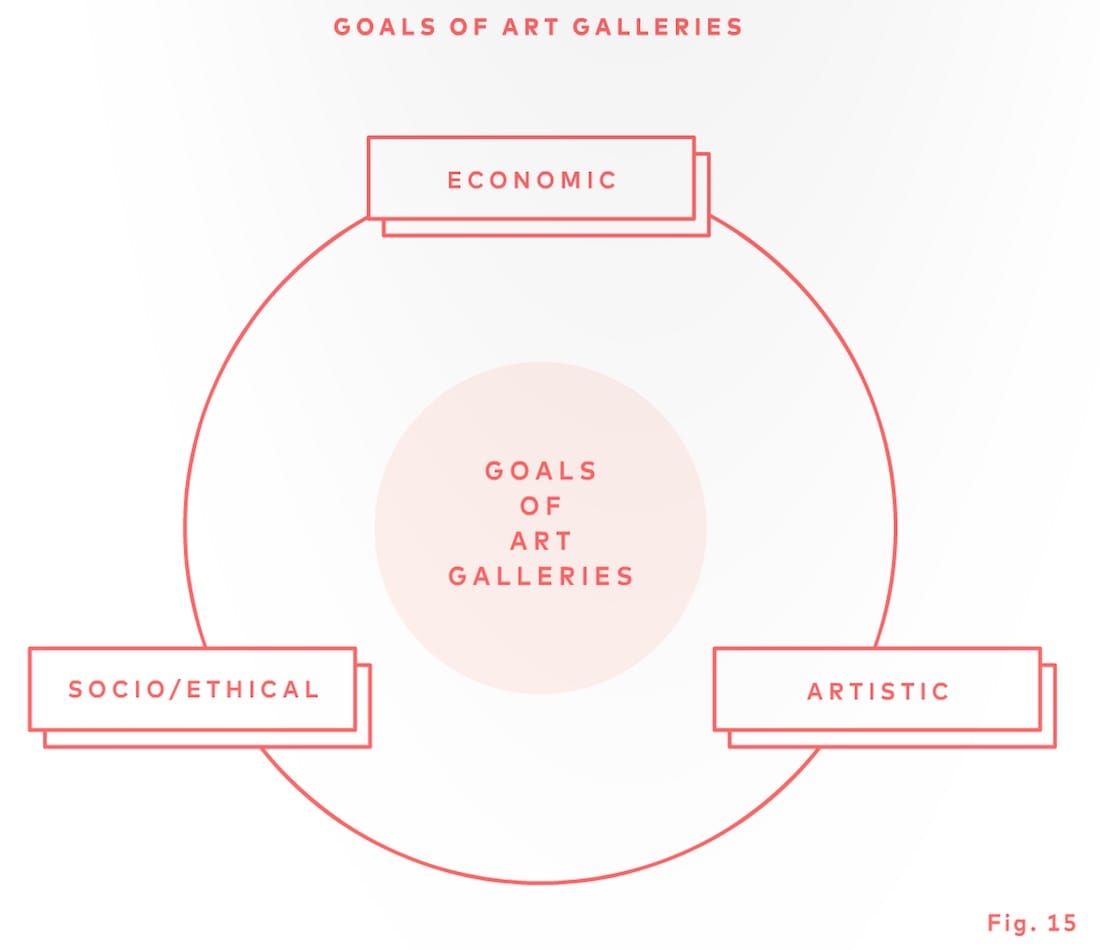

I agree with Magdalena’s take on the socio-ethical continuum of Resch’s “Goals of Art Galleries” graph (figure 15), that artists are not here to feed the art-industrial complex, but are here to be fed by that system — however imperfect and fucked up the model remains. Clearly there is much work to be done around issues of equity in the art world, including greater representation of women and people of color, but I don’t think we can look to management to solve the problem that begins with a consumer base of 70% male collectors. (Unless you think Gagosian’s plan, cited by Resch, to employ a 75% female staff to deal with those men is a reasonable competence configuration.) I’m also deeply suspicious of Resch’s directive to simply market art to the next generation of the privileged elite through edutainment and happy hours as a solution to an aging collector base.

7. Conclusion

“However, in the end it is the gallery owner who creates demand through identification and opportunity and not by blindly following the market. Gallery owners must always keep in mind that continual customer orientation would mean little or not creative development” (italics mine). I think this passage, from Resch’s two-page conclusion — not much is to be concluded after 10 years of research and application, apparently — is perhaps the most important takeaway from the book. It not only describes Resch’s plan for art, but the danger dealers and artists face in being sucked into the gravity well of the market. As Artslant editor Joel Kuennen once told me, “the art market has fucked us all.”

Magdalena and I both suggest skipping Resch’s corporate seminar and taking some time to re-read New York State’s Consignment Laws, which can be found here, as well as this memo from the New York State Bar Association on consignment law for artists. The latter states: “Commissions usually range from 10% to 50% and it is not uncommon for galleries to receive 40% to 50% for works consigned by artists.” We suggest artists and dealers follow Edward Winkleman’s advice and acknowledge the symbolic and practical importance of the 50/50 split, which reflects a commitment to something much more complicated than “financial performance.” I’d love to read a book called “The Public Funding of Art Spaces,” but for now I’m ready to support the efforts of WAGE’s resale royalty working group around policy and contracts that respect artists’ roles in producing enormous value for so many other people. Nobody without land and title in Europe, a trust fund, vast holdings of gold, or parents who were also art dealers should use Resch’s book as a manual for starting and running a gallery.

Magnus Resch’s Management of Art Galleries is available from Hatje Cantz.