“Your Money Is Safe in Art”: How the Times-Sotheby Index Transformed the Art Market

In 1967, Geraldine Norman was tasked with leading an editorial collaboration between the London Times and Sotheby’s. The project galvanized the conceptualization of art as an investment asset.

“Works of art have proved to be the best investment, better than the majority of stocks and shares in the last thirty years.”

This was the confident declaration of Peter Wilson, the then chairman of Sotheby’s, during his 1966 appearance on the BBC’s Money Programme. Though he was only eight years into his chairmanship, Wilson had already overhauled the fusty image of the art trade. His ingenious pre-sale marketing efforts, celebrity invitations, and black-tie sales had transformed Sotheby’s auctions into major news affairs, and deepened the perception of Christie’s as an antiquated rival.

Reacting shrewdly to the post-war wave of prosperity, Wilson was determined to bring newly moneyed buyers into the fold. He sought to convince businessmen and bankers that collecting was no longer the exclusive preserve of cultured, old-money dynasties such as the Rothschilds, Rockefellers, or Mellons. Crucially, Wilson wanted to instill the notion that art can be an investment. The sudden and precipitous rise of the Impressionist art market during the 1950s may be cited as proof of this. If you inherited an Impressionist painting, you could now sell it for vastly more than your family paid to acquire it. Wilson’s idea just needed to be packaged in an immediate and compelling fashion.

A year after Wilson’s television appearance, twenty-seven-year-old Geraldine Keen — now Geraldine Norman — received a letter in Rome. A graduate of Oxford University and UCLA, Norman had left her job as an editorial statistician for the Times newspaper in London to work for the Food and Agriculture Organization of the UN. The letter was a job offer from the paper’s City editor, George Pulay, asking Norman whether she would consider returning to London. He wanted her to spearhead a new editorial collaboration between the Times and Sotheby’s.

* * *

Few people active in the art world today have heard of the Times-Sotheby Index. Those who have are most likely veteran art dealers or retired auction staff. Web results primarily consist of library entries for Norman’s 1971 book on the project.

Published regularly in the Times between 1967–1971, the Times-Sotheby Index purported to chart the changing prices of art sold at auction. Each feature centered on a single movement or department (Impressionism, English silver, Chinese ceramics, etc.) and were accompanied by charts that illustrated sales prices from the early 1950s to the present.

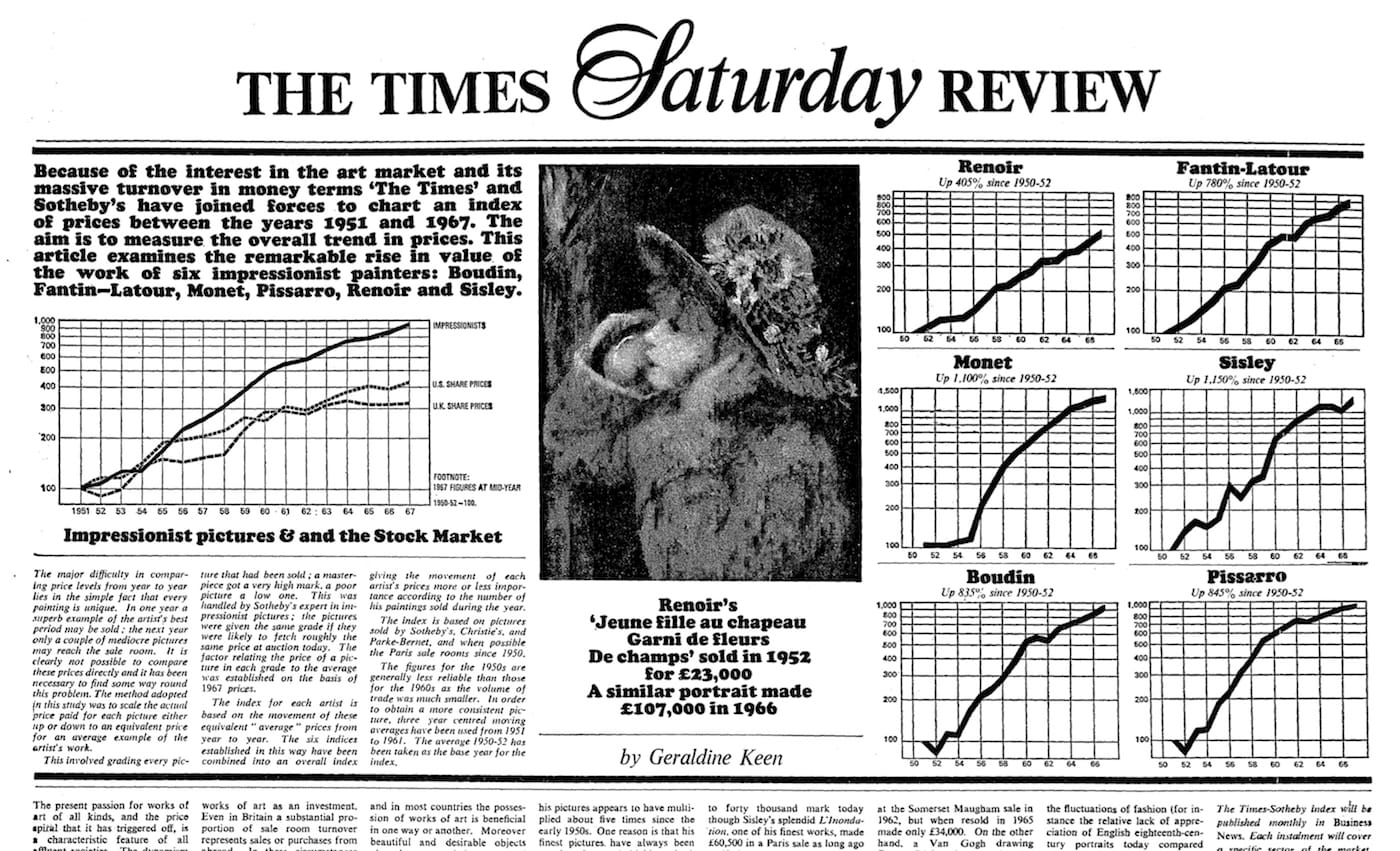

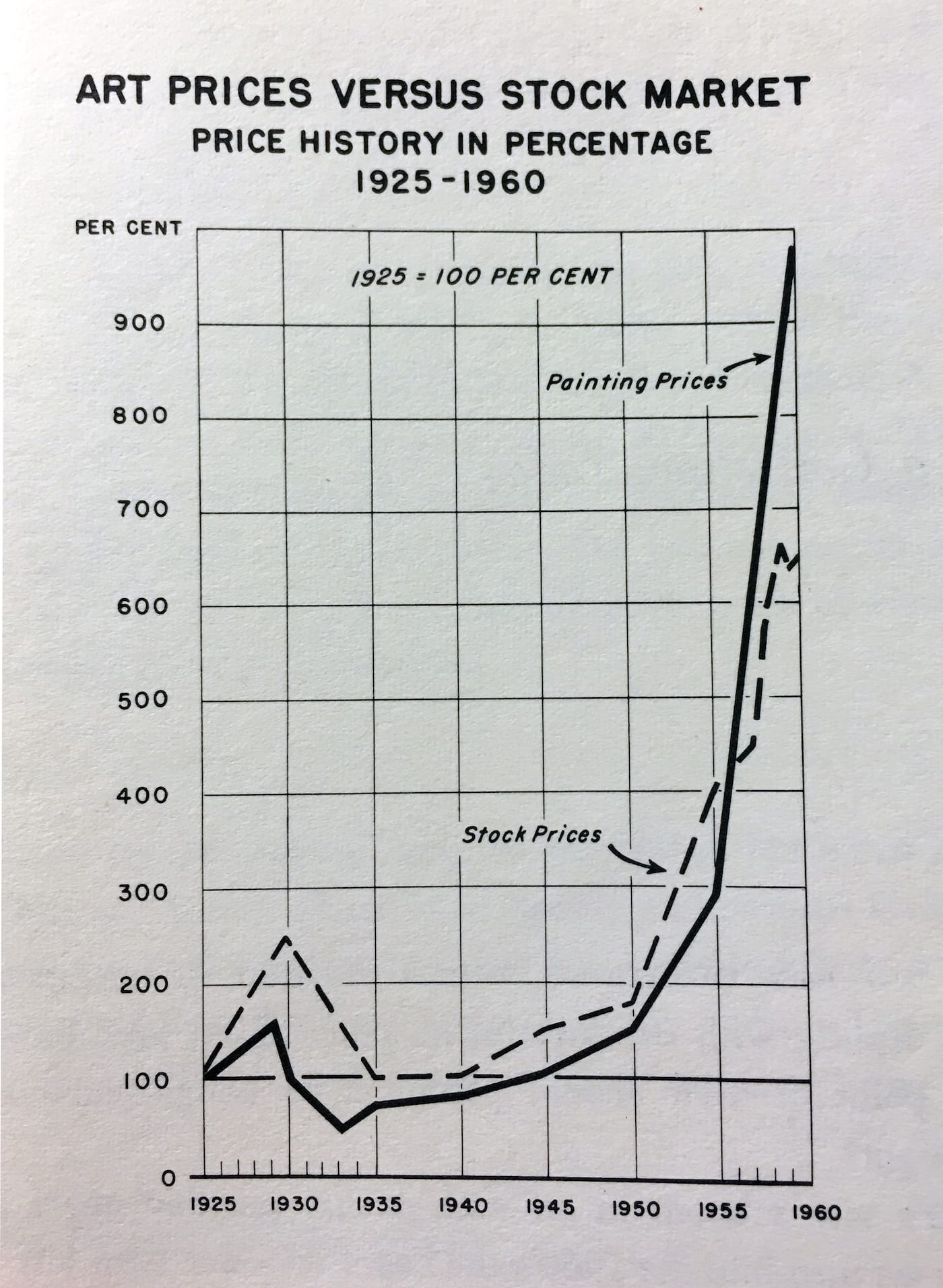

The first index, published on November 25, 1967, includes seven prominent graphs dedicated to Impressionism. Six charted the prices paid for specific artists since 1950–52: Renoir (“up 405%”), Fantin-Latour (“up 780%”), Monet (“up 1,100%”), Sisley (“up 1,150%”), Boudin (“up 835%”), Pissarro (“up 845%”). The seventh graph includes three indices, the value of Impressionist paintings, US share prices, and UK share prices — the former vastly outpacing the latter. The message was clear: Art is a hot commodity, and its sale value can and should be conceived in much the same way as a stock on the Dow Jones or FTSE 100.

The market for contemporary art has grown exponentially since the 1960s. It’s now commonplace to describe the intricacies of an artist’s particular “resale value,” or “collector base.” Innumerable artworks reside out of sight within heavily secured free ports, where their owners avoid custom duties. The press routinely report record sales, rehashing features on the best-selling artists and publishing listicles on the world’s most expensive works. Companies such as Artnet, Collectrium, Artprice, and ArtRank sell their data and insights on sales and trends. Speculation is the norm. However, in 1967, the Times-Sotheby Index’s brazenly analytic conception of art’s value was, with a few exceptions, unprecedented and highly radical.

“Our culture has been schooled to think of works of art as investment commodities,” wrote Robert Hughes in his renowned 1984 essay, “Art & Money.” “The art market we have today did not pop up overnight … I think of it as beginning with a curious enterprise called the Times/Sotheby Art Indexes.” The critic continued:

Perhaps it was the graphs that did it. They gave these tendentious little essays the trustworthy look of the Times financial page. They objectified the hitherto dicey idea of art investment. They made it seem hard-headed and realistic to own art.

The index was reportedly conceived during a lunch between Pulay, Wilson, and Brigadier Stanley Clark. As Sotheby’s PR agent, Clark had played an instrumental role in the company’s 1964 acquisition of Parke-Bernet auction house, which vastly expanded Sotheby’s presence in the US. (Christie’s did not open its own sale room in New York until 1977.)

Together, Clark and Wilson landed a spectacular PR coup in convincing the Times to collaborate on the feature. The name alone guaranteed a tranche of regular free press for Sotheby’s and the association with the Times instantly bestowed authority on the index’s findings. Though they conceived it, neither Wilson nor Clark actually brought the index to life. That responsibility fell squarely on Geraldine Norman’s shoulders.

I interviewed Norman, now 78, over the phone. By her own admission, the project did not get off to a smooth start. “I was worried because I thought art actually can’t be valued and that it’s ridiculous to put prices on things and measure them in an index,” Norman told me. “I panicked all one night and at the end of it I decided, well … I may as well do it.”

The project presented an obvious methodological conundrum. Unlike gold or oil, art is not a singular commodity. Every piece is unique, and an artist’s oeuvre will always be comprised of works judged to be of a comparatively higher or lower quality. Aesthetic judgements, regardless of trends or received wisdom, are subjective. Condition, provenance, and size are just a few of the factors that have a bearing on how an artwork is appraised.

Tracking the prices of every Impressionist painting sold at auction would be an unmanageable task, so Norman’s solution was to compromise. For the first index, she focused on six “representative” painters. Monet and Renoir stood as the movement’s perceived masters, while Fantin-Latour and Boudin represented lesser “companions.”

Norman then deferred the issue of quality and variance to a Sotheby’s specialist, who divided up each artist’s oeuvre into groups of “roughly equal intrinsic value,” or as Norman jokingly put it, “from masterpiece down to crap.” To do this, Norman would sit with the relevant specialist and review the sale records for each artist documented by the auction house. Having determined her parameters, Norman tracked the prices paid for each artist before combining the results into a single index. “The method adopted in this study,” Norman announced in the Times, “was to scale the actual price paid for each picture either up or down to an equivalent price for an average example of the artist’s work.” The data included pictures sold by Sotheby’s, Christie’s, Parke-Bernet, and “when possible, the Paris sale rooms since 1950.”

Norman’s method had a number of inherent shortcomings. It functioned on the assumption that the value of one example of an artist’s work would remain a constant multiple or fraction of the value of any other, unaffected by the realities of changing tastes or demands. More Renoirs might be sold in one year than another, and of those works, some could far exceed or fall short of expected auction prices. An exceptionally cheap or expensive painting would register on a graph as a sudden downturn or surge. To avoid this, Norman excluded so-called masterpieces, which would likely fetch exceptional prices. Another major criticism leveled at the index was that it could only provide an approximate insight into auction prices. Private transactions, and sales by galleries and dealers — by far the bulk of the art economy — were excluded. It was also invariably problematic that a Sotheby’s specialist would have say over which works were and were not “representative.”

Norman was entirely upfront about these limitations, many of which she discussed in the article accompanying her first index. It’s clear that she was sincere about making the best of a near impossible assignment, but she also understood the genius of Wilson’s vision. “It was [his] brilliance that he saw how it could affect his sales figures,” Norman told me. “I don’t think I saw it at the time as promotional [but] it worked as a Sotheby’s promotion.”

* * *

The conceptualization of art as an investment commodity was not without precedent. Émile Zola’s 1886 novel, L’œuvre (“The Work” or “The Masterpiece”), characterized the increasingly speculative character of the late- nineteenth-century art market. The novel features a character named Naudet, a Parisian art dealer who only engages with the “moneyed amateur” who buys pictures “as he might buy a share at the stock exchange.” Naudet’s sales pitch is as follows:

“Look here, I’ll make you a proposal; I’ll sell it you for five thousand francs, and I’ll sign an agreement to take it back in a twelvemonth at six thousand, if you no longer care for it.”

After that Naudet loses no time, but disposes in a similar manner of nine or ten paintings by the same man during the course of the year. Vanity gets mingled with the hope of gain, the prices go up, the pictures get regularly quoted, so that when Naudet returns to see his amateur, the latter, instead of returning the picture, buys another one for eight thousand francs. And the prices continue to go up, and painting degenerates into something shady, a kind of gold mine situated on the heights of Montmartre, promoted by a number of bankers, and around which there is a constant battle of bank notes.

Naudet’s approach, and those of the dealers on whom he is likely based, prefigured the market manipulation we recognize today, an example being the auction phenomenon of “flipping.” The nineteenth-century art market is wonderfully illustrated in Philip Hook’s Rogues’ Gallery, which includes a chapter dedicated to Paul Durand-Ruel, the innovative art dealer who championed the Impressionists. As Hook observes, Naudet’s approach can only function if a dealer establishes a monopoly for an artist’s work, and Durand-Ruel operated shrewdly in this regard. “I am entirely disposed to take all your paintings,” wrote the dealer in a letter to Pissarro. “It is the only way to avoid competition, the competition that has prevented me from boosting your prices for so long.”

Norman was also not the first to demonstrably equate auction sales to stock values. In 1961, art collector Richard H. Rush published Art as an Investment, a beginner’s guide to collecting. Each chapter included graphs dedicated to the changing sale value of different schools of art.

Rush’s methodology was strikingly similar to Norman’s, the key difference being that the collector limited his data to “medium” sized paintings that would be “a convenient size to hang on the wall.” Buried in one of his chapters, with little fanfare, is an additional graph comparing stock prices to auction sales. “Despite the bull market in stocks after the 1957 recession, paintings forged far ahead of the stock market to the year 1960,” wrote Rush, “and despite the setback in the stock market in that year, painting prices still rose.” Norman said she was unaware of Rush’s work. “That’s shaming. I should have known about it, but I didn’t.”

Despite its title and graphics, Rush’s book is not a full-throated endorsement of art as a commodity asset. The collector’s guide champions studiousness, patience, and above all, a life-long commitment and passion for art.

The important collectors of paintings usually do not sell. They look upon their paintings as their treasure and a major love of their lives to which of course a price tag can be attached but which usually need not be turned into cash during their lifetimes. It is enough to know that the value is there and that it can be passed on to heirs or public institutions as their contributions to the culture of society.

Norman’s headlines during the late ‘60s were less equivocal. “Your money is safe in art,” the journalist declared in June 1968. “Fine art treasures are a truly convertible currency and will maintain their value on the international market.”

Unsurprisingly, the index attracted the ire of readers, critics, and other arts professionals, many of whom wrote to the Times. One such letter was published in October 1968. “The Times Sotheby Index … represents the very height of vulgarity and crass commercialism,” wrote L.J Olivier of Coggeshall, Essex. “One day, please God, the tide will turn. The air conditioned vaults of philistine businessmen will be broken open and the contents expropriated and your wretched art journalists will be stoned to death with fake Etruscan bronzes.” “Paeans of praise be to Mr. L. J. Olivier,” James R. de la Mare of Woodchester, Gloucester, responded. “An era in which, say, a Raphael is less a masterpiece than a ‘hedge against inflation’ deserves the choler of your correspondent and, perhaps, shames us all.”

Art dealers were also incensed by the index. “I remember Sir Geoffrey Agnew being particularly angry about it,” Norman told me. “He certainly expressed it to me personally. Somehow, I added him into the Index and he was happy, but I can’t remember how I did that. The sales pitch said art has a wonderful, intangible value — that it is above the whole sordid commercial world. I think [dealers] believed that. Sir Geoffrey did anyway.”

Carmen Gronau, the head of Sotheby’s Old Master department concurred. “She said, ‘it’s a nonsense game; you can’t do it with old masters,’” Norman recalled. “‘You’re not going to have an old master index.'” Peter Wilson’s reaction was emphatic. According to Norman, Wilson sat Gronau down with a bottle of whisky and a stack of sales records. After months of evasiveness and a late night’s work with Norman, the specialist reluctantly settled on the schools and artists they thought ought to be incorporated into an Index. Julian Thompson, the head of the Chinese art department and a mathematician, also had reservations. “I think it’s pretty suspect,” he reportedly told Norman, “but I can see what you’re doing.” Aside from procuring whiskey for Gronau, Norman maintains that Wilson never sought to influence or interfere with her work. “He watched from afar with deep interest.”

The opposition to art’s evolving commodity status directly impacted the production of Norman’s 1971 book. The journalist’s UK publishers rejected her proposed title, Art and Money: A Study Based on the Times-Sotheby Index, opting for the slightly more sober The Sale of Works of Art instead. Only US editions bore Norman’s intended title.

In a scathing review entitled “In Sotheby-land the graphs go up,” New York Times critic Grace Glueck dismissed Norman’s methodology as a “complex maze of simplistic reasoning.” “I heartily recommend [the book] to those who collect not art, but money,” she wrote, “and can afford to shell out $20 for [what] is really nothing more than a cumbersome advertisement for Sotheby’s.”

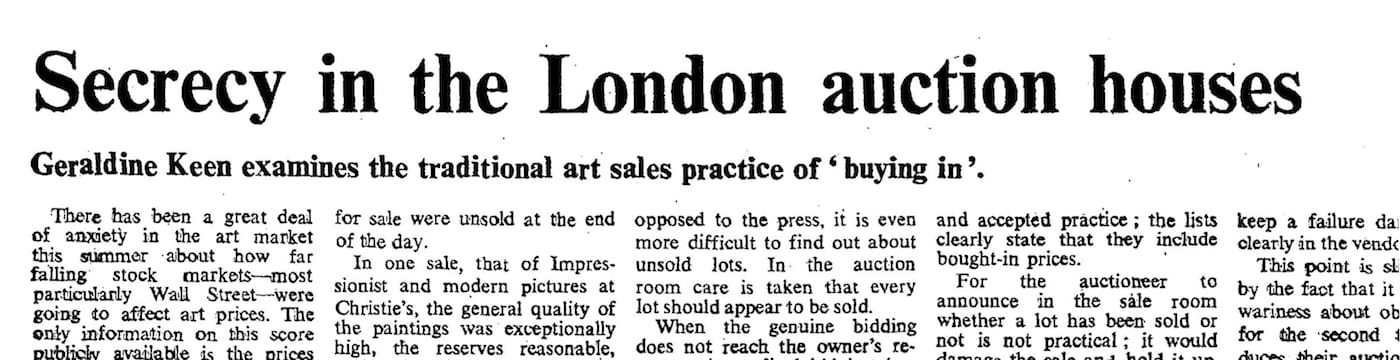

As part of her critique, Glueck observed that Norman had not identified the percentage of works that were “bought-in” below their reserve price, the undisclosed minimum bid at which a consignor is willing to sell their work. If the auctioneer fails to attract bids higher than the reserve, then the work is unsold (i.e. bought-in or “passed”). In lieu of real bids, auctioneers will conjure imaginary ones in order to surpass the reserve price (a practice known as “chandelier bidding”). At the time, neither Christie’s nor Sotheby’s publicly disclosed the percentage of bought-in lots, thereby maintaining the illusion of unrelenting demand. Glueck also chided the fact that the Times promoted Norman to sale-room correspondent amidst her ongoing work with the index. “[I] wonder how Christie’s, Sotheby’s London rival, likes that?” the critic reasoned.

Glueck’s criticism of Norman’s conflict of interest, though fair, proved to be misplaced. By 1971 — the very year Art and Money went to print — Norman’s professional relationship with Wilson had evaporated, and she was held in equal contempt by Peter Chance, the chairman of Christie’s. Ironically, it was Norman’s determination to shed light on auction reserves that marked the death knell of the index.

* * *

The standard narrative is that Wilson scrapped the Times-Sotheby Index after auction sales began to dip. Indeed, the last feature to be published, headlining “English silver’s lacklustre market,” could hardly be described as a press coup for Sotheby’s. Norman’s feature had documented a few price declines over the years (“No rags to riches story for English porcelain,” November 1968; “Fall in Chinese ceramics,” September 1970), but the truth of its demise is far more complex.

During the Summer of 1970, Norman informed Wilson and Chance that she was writing a critical article on the secrecy surrounding bought-in lots. Norman observed that fictitious names (some of which were pseudonyms used by secretive bidders) regularly appeared on the sale lists distributed to subscribers. Only later did the practice become widely known. “We would go behind a curtain after every sale,” Fiona Ford, a former Sotheby’s press officer, later relayed to Philip Hook, “and find out from Peter Wilson what we were expected to lie about.”

Much of what Norman told me is corroborated by John Herbert’s 1990 memoir, Inside Christie’s, which delved into the journalist’s falling out with Wilson and Chance. Herbert, an ex-journalist who worked as Christie’s PR director between 1959 and 1985, was shocked by the industry’s “economy with the truth.”

It’s true that we didn’t volunteer information on bought-in lots, if we weren’t asked about them, and the standard procedure was that the total given would be the knock-down and include bought in lots. Geraldine, once she was confident of her position, decided this was not good enough; she wanted, certainly when it came to important sales, every price in the catalogue and whether the work was sold and if so who the buyer was. With this information she could work out the percentage sold and bought in. It was strange that no other journalist had ever asked for such basic information before.

Norman, who had so keenly propped up art’s burgeoning investment status, was now deploying her expertise in a bid for greater market transparency. Predictably, her queries were not well received by Wilson or Chance. The chairmen met with the Editor of the Times, Sir William Rees-Mogg (father of Conservative MP and ardent Brexiteer Jacob Rees-Mogg), in an effort to quell her story. As Norman told me:

They were both outraged. The obituaries editor told me that it was not a question of a two-faced villain, but a four-faced villain, because each of them came with their deputy. Rees-Mogg listened to them and then he said quietly, “gentlemen, I’m sorry but I think this is a matter of public interest. We will be publishing her article.”

Peter Wilson never forgave me for that. He felt that I had let the side down, that it was disloyal. He first said that he was going to close the doors of Sotheby’s to me, that I was never to be allowed into Sotheby’s again, but he actually couldn’t do that because I was the Sale-room Correspondent of the Times [laughs]. When we met, he used to shake with anger.

On July 16, 1970, the Times published Norman’s article, “Secrecy in the London auction houses.” Eight months later, the paper published her final Times-Sotheby report.

Norman’s July article exposed the use of fake names, but also outlined the defense for such secrecy. Auctioneers maintain that if bidders knew reserve prices, they would be disinclined to bid beyond them. Works known to have been bought-in might be perceived as undesirable and can therefore be harder to resell. Yet, such secrecy runs entirely counter to the ethos of the public auction. “The auction rooms have profited greatly from the public and open nature of their transactions,” wrote Norman. “Their secrecy over unsold lots is thus something of a contradiction.” In the face of increasing scrutiny, the auction houses gradually amended their policies. By 1975, both companies excluded bought-in lots from their sale lists.

“Few journalists can claim, as [Norman] can, to have forced two world famous firms to change their hallowed practices by sheer persistence and strength of mind,” wrote Herbert.

I remember our first meeting. I saw this small girl get out of a battered German bubble car, dressed — I hope she will not think me ungallant — rather like one of Augustus John’s gypsies, with wisps of hair flying in all directions.

According to Herbert, Chance became obsessed with Norman. “There’s nothing, in my opinion, which is not beyond the line of duty when it comes to controlling that woman,” he reportedly snapped. The Christie’s chairman ordered Herbert’s department to analyze Norman’s auction coverage and determine the extent of her bias for Sotheby’s. The report concluded that Norman had in fact given Christie’s approximately 24% more coverage, a finding that Herbert attributed to the pre-sale exclusives he regularly touted her. “More time was spent on discussing what to do about Geraldine at board meetings than on any other one subject.”

By 1974, it’s clear that Norman’s opinion on art’s commodity value had cooled considerably. “There are and always will be marvellous opportunities for speculation in the art market,” she wrote in an article examining British Rail’s art investments, “but the idea that art is a solid and safe investment medium is a fallacy.”

In 1987, Norman left the Times to join the Independent, where she worked until 2000. The journalist has published numerous books, including a critically lauded history of the State Hermitage Museum. As a result of the project, Norman later became Director of the Hermitage Foundation UK, a registered charity dedicated to fundraising and cultural exchange. “It’s very eccentric,” Norman remarked about her career, “but it all hangs together.” Despite their falling out, Norman spoke admiringly of Wilson. In Art and Money, she credited his chairmanship with building the “most dynamic auctioneering complex in the fine-art market.” “I would hasten to say I think he was charming and a genius,” Norman told me. “I was very sad when he took against me because it had been great fun working with him.”

By the time Art and Money was published, the findings of the Times-Sotheby Index had been syndicated in publications around the world, including the New York Times, Süddeutsche Zeitung, and Connaissance des Arts. Two years later, collectors Robert and Ethel Scull sold works from their contemporary art collection at Sotheby’s Parke-Bernet for a staggering profit, definitively shifting the market’s focus to contemporary art.

Robert Scull, a consummate self-promoter, keenly stressed the disparity between the prices he and Ethel originally paid with those they had fetched at auction. Robert Rauschenberg’s “Thaw” (1958), which the couple bought directly from the artist for $900, sold at the auction for $85,000. The extraordinary mark-up in prices inspired the now pervasive model of buying new work and holding out for a profit. Though the Scull auction is routinely cited for cementing this line of thinking, it was the inexorable logic of features such as the Times-Sotheby Index that catalyzed it. “It proved a self-fueling engine,” wrote Philip Hensher in 2006. “By demonstrating that pictures could be thought of in this way, the index guaranteed that they would be.”

“I think it was the starting point because it was so blatant,” Norman remarked.

Picasso up 3 points, Renoir down 2. It didn’t strike me that it was having an immediate impact on the art market. It changed people’s minds and way of thinking, but it took a matter of years to work its way through. It was only ten years later that I began to realize that it had actually made a sea change in buyers. It was a gradual thing.

John Herbert’s conclusion was firm. “No one journalist had such an impact on the art market from 1967, whether on auction houses, museums, or members of the fine art trade as Geraldine.”